The Chinese New Year was celebrated in early February and enter the year of the monkey. After the celebration the Chinese stock market rallied in true New Year’s fashion. Their enthusiasm spread to both the European and U.S. stock markets giving the world a much needed boost from the current pullback.

All the recent attention to China reminds me of a fabulous Chinese Proverb. “The best time to plant a tree was twenty years ago. The second best time is now.” When advisors and clients inquire about the best time to buy stocks or invest money, a confident and truthful response can always be “the best time to invest was twenty years ago, the second best time is now.” The twenty year time horizon gives the proper perspective to a long-term mission. The proverb also instills hope. Long-term goals can be achieved if you start the process and stay committed.

The January stock market sell-off continued into early February. By the eleventh day, U.S. stocks bottomed and mounted a rebound turning negative results into flat returns for the month. International stocks followed a similar path and posted small declines in February. One thing for sure this year is higher volatility. Triple digit moves on the Dow Jones Industrial Average is now commonplace. This trend is likely to continue as the Federal Reserve charts a globally divergent course on monetary policy, oil prices remain uncertain, currencies are in flux, economic growth is fragile, geopolitical risks run high and the 2016 election cycle appears to be one for the ages. Expect volatility to remain high this year.

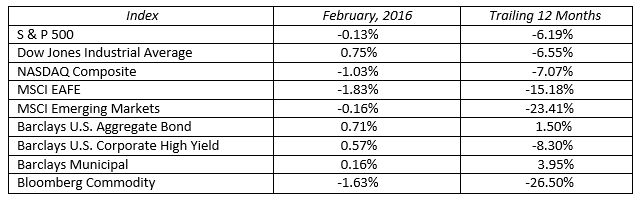

U.S. stocks finished mixed for the month as larger capitalization stocks outperformed smaller capitalization stocks. The S&P 500 and NASDAQ Composite finished down 0.13 and 1.03 percent respectively, while the Dow Jones was up 0.75 percent. International stocks as measured by the MSCI EAFE and Emerging Markets were down fractionally at 1.83 and 0.16 percent. New leadership emerged from the defensive sectors as utilities, metals and mining and consumer staples led the market back to flat for the month.

The equity market rebound pumped life back into credit sensitive bond sectors. High yield bonds, battered from the recent flight to quality trade, reached valuations too cheap to ignore. The February wide credit spread mark (as measured by the Bank of America Merrill Lynch US High Yield Master Spread) reached 8.87 percent on the day stocks traded at their monthly lows. In the last two and a half weeks, high yield spreads tightened over one hundred basis points bringing high yield bond prices back to their monthly starting point. This is good news for bond investors.

The 2016 bond market will provide relative cover for those investors looking for a break from higher volatility. Expect one 25 basis point Fed rate hike in the second half of the year and overall interest rates to remain low, just as they did last year. One to three percent total returns should be your bond market expectations from here.

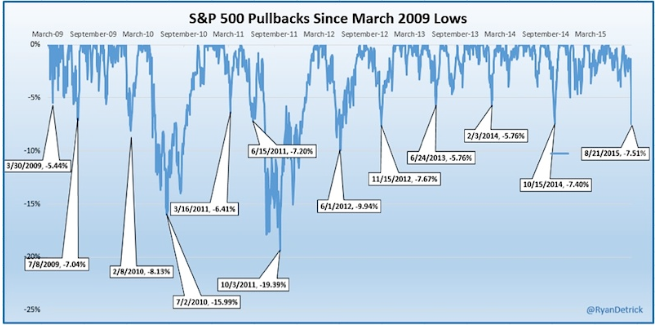

A closing thought in the face of higher market volatility. It is important to remember capital markets do not move up or down in straight lines. Since March, 2009, the stock market rally has been quite remarkable. Along with success, comes regular price pullbacks along the way. The recent 10.4 percent pullback is no exception. As you can see below there have been thirteen other pullbacks as the S&P 500 journeyed from 666 to 1,932 over the past seven years.

The secret to the long-term success of planting trees twenty years ago is the commitment to leave the trees in the ground for the entire time. The secret to the long-term success of investing is the ability to stay invested for the entire time. Unfortunately, every market pullback becomes an emotional challenge to your financial commitment. Since it is the year of the monkey, take the monkey off your back and keep your investments planted for the long haul.

MARKETS BY THE NUMBERS:

To expand on these Market Commentaries or to discuss any of our investment portfolios, please do not hesitate to reach out to us at 775-674-2222