Stocks had a dreadful start to the year only to rally back to within sight of the all-time highs reached one year ago. May was preceded by the best two-month gain since 2012, but the recent price momentum faltered as political and economic concerns weighed on the market. We appear to be at the point in the cycle where investors are seriously debating the market’s next move. The old adage, “Sell in May and go away”, is timely as we enter the summer months where June and August have historically been the two weakest months of the year. The $64,000 question is: Does the price momentum continue and take us to new highs or is another correction coming?

The first place to search for an answer to this question is corporate earnings. The consensus earnings per share (EPS) growth estimate for 2016 has been falling steadily this year and now stands at +2.3%, down from an earlier expected +6.8%. The positive earnings growth is expected to arrive in the second half of the year. With earnings growth expectations low and a new tailwind beginning to blow from higher oil prices, positive earnings surprises may be on the way. On the other hand, S&P 500 valuations are stretched as the trailing price/earnings ratio is nearly 18 times. The equity market has an optimistic outlook for third and fourth quarter earnings and if achieved, the market’s current valuation will be validated. If future earnings disappoint, then prices will need to correct. As a result, this is likely an appropriate time to temper your near term return expectations.

In addition to earnings and valuations, the market also needs to consider the Fed’s intention to raise interest rates in June. This is not a foregone conclusion, but the impact of a Fed move has to be handicapped as it affects a wide variety of market factors: the value of the U.S. dollar, future economic growth, consumer spending, the yield curve, mortgage rates and commodity prices. On the economic front, U.S. employment data disappointed investors as 160,000 jobs were created in April, the smallest gain since September and 40,000 short of expectations. Weak overseas manufacturing numbers from China, UK and France sent international stocks down while Brittan’s debate over exiting the European Union created further uncertainty.

Volatility has been stable the past few months, but as the market is coming to grips with all of the aforementioned issues we expect it to reappear. The political environment leading up to the Democrat and Republican conventions in July adds further uncertainties. Expect volatility to increase as the market moves through the summer season and digests a lot of new information.

In every monthly commentary our goal is to provide some factual information and insight into the markets. While we may discuss what happened last month and outline our expectations for the next month or quarter, please remember financial success is measured in years, not week-by-week or month-by-month. There is no substitute for establishing long-term financial goals with an understanding that markets will go up and down from one period to the next. Don’t play the monthly swings. The game is won by consistently playing the long-term trend. Stay committed to your 5 or 10-year plan and stay invested.

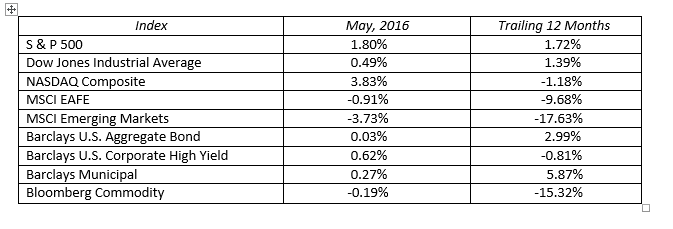

MARKET BY THE NUMBERS:

To expand on these Market Commentaries or to discuss any of our investment portfolios, please do not hesitate to reach out to us at 775-674-2222