The year was a tale of two markets. The first six weeks belonged to the bears, and the last six weeks the bulls were in charge. The bulls had the final say once again.

The year got off to a rough start as major stock indices were down double digits, reaching their eventual low water mark for the year. The Dow Jones Industrial Average bottomed at 15,450, the S&P 500 hit 1,810, the yield on the 10-year U.S. Treasury was 1.63% and oil was $26.19 per barrel. Fast forward to the post-election euphoria and we almost saw Dow 20,000, the S&P 500 hit 2,270, the 10-year U.S. Treasury yield north of 2.50% and the price of a barrel of WTI crude settled in the $50 area. What a difference 10 short months can make.

The election provided a new coach with a new playbook. The market obviously likes what it is hearing, but the new team has not taken the field yet. The new playbook has plans to be pro-business with lower taxes, less regulations, reformed health care, energy independence and a keen focus on growth and jobs. The plan on paper looks great, but it still needs to be executed on the field with opponents fighting hard at every turn. The market has given us a glimpse of what could be, but keep in mind the market will eventually trade on what will be.

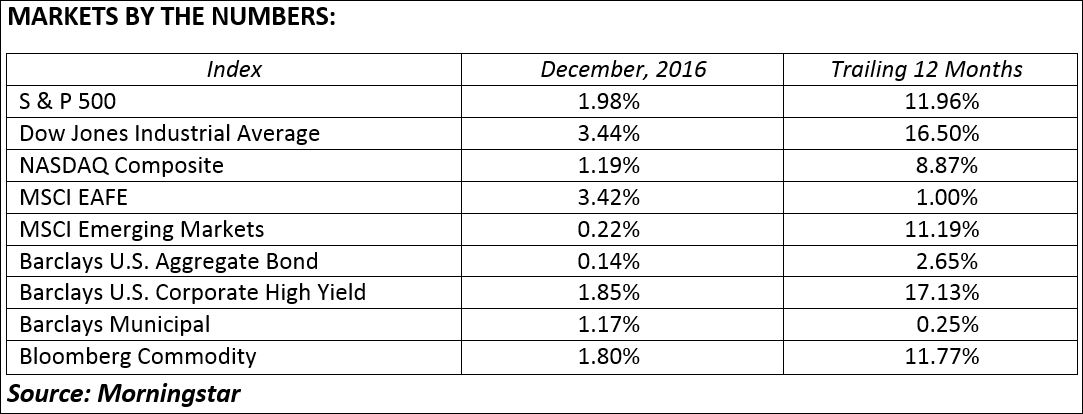

After a gut wrenching start, stocks turned the corner and produced solid returns this year. The Dow Jones Industrial Average gained 16.50% for the year, the S&P 500 was up 11.96%, and Emerging Markets delivered 11.19%, while MSCI EAFE added just 1.00%. The big stories for stocks this year was the turnaround in oil prices, low interest rates and the beginning of an earnings recovery. The prospect of a new pro-growth political environment added to the bullish momentum.

Bonds generally moved in opposite directions from stocks this year. Bonds rallied early in the year as oil prices collapsed and it became apparent the Federal Reserve was not going to raise interest rates at the pace they themselves had projected. The post-election stock rally negatively impacted bond prices as the Federal Reserve is now in play and increased economic growth may pave the way to higher rates.

If the economy begins to grow faster, expect interest rates to move higher in an orderly fashion. For the past two years the Fed told us they expected to raise the Fed Funds rate four times at 25 basis points in each year. Their eight forecasted rate hikes became one 25 basis move in 2015 and one in 2016. This will likely be the year when we finally get the four 25 basis point hikes. This is not all bad news, just reflective of a stronger economy where the Fed finally has room to maneuver.

Bond investors will need to prepare their portfolios and their expectations for a new world of gradually higher interest rates. Defense in bonds will be the name of the game. Short duration, floating rate notes, TIPS and asset-backed securities should provide the best opportunities in 2017. Own bonds to diversify your overall portfolio. Positive low-single digit returns would be the best outcome next year, and slightly negative returns would not be a surprise.

The New Year may see some consolidation from the post-election rally. If it comes, don’t be tricked into thinking it is the beginning of the end. Economic optimism and higher corporate profits fuel rallies. Our forecast is for 5-10% upside in equities next year with bonds struggling to produce positive returns. Stay positive, stay invested.

To expand on these Market Commentaries or to discuss any of our investment portfolios, please do not hesitate to reach out to us at 775-674-2222