The positive stock market momentum continued throughout the month as economic and earnings news advanced equity prices to multiple all-time record high levels. As always, some individual companies exceeded earnings expectations and others fell short. In aggregate, the good news regarding company earnings and economic data outweighed the bad moving stock indices ever higher. The bond market experienced a sideways month as interest rates initially moved higher and then came back to levels slightly above where the month started.

The U.S economy is deriving its strength from the consumer and the service sectors while manufacturing sector has been a drag on growth. The good news here is that most U.S. companies provide services rather than manufacture products. The Institute for Supply Management’s Purchasing Managers Index for non-manufacturing firms rose nearly two points last month to 54.7 demonstrating service sector strength.

Retail sales advanced 0.3% in October, according to the Department of Commerce. That surpassed the 0.2% gain forecasted by economists. The consumer is employed and continues to spend. The economy added 128,000 jobs in October, far surpassing the 85,000 expected. Unemployment ticked up to 3.6% reflecting more people entering the job market. Existing home sales improved 1.9% last month and year-over-year sales were up 4.6% through October. Building permits for new homes are at the highest level since 2007 showing further proof of a strong consumer sector.

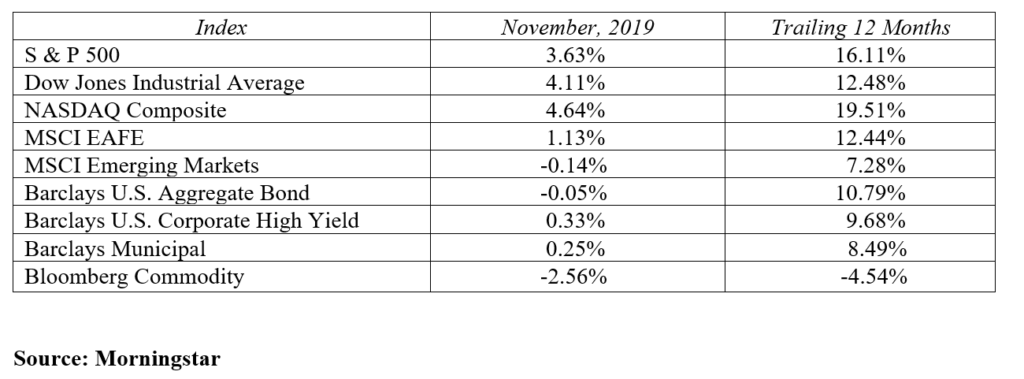

What a difference a year makes. One year ago the stock market was in the middle of a painful fourth quarter correction. After the 13.5% price correction, the Federal Reserve came out in early 2019 verbally changing their plan on monetary policy. The combination of lower stock prices and a new Fed outlook set the stage for a gangbuster 2019. The 2019 rally continued in November as the major stock market averages closed the month about 4% higher. The Dow Jones Industrial Average reached and closed the month above 28,000 for the first time. International stocks did not keep pace with the rally in U.S. stock markets this month.

The S&P 500 closed at new record highs twelve times over the course of November, 2019. Stock valuations are typically measured by price-to-earnings (P/E) ratios. These ratios now show U.S. stocks trading at 18 times forward earnings which are at the upper end of recent ranges. This means stocks are somewhat expensive on a relative basis. This may set the stage for a future 5-10% price correction, which if it happens should not surprise investors. Remember, stocks appreciate over time but they do not go up all the time. We still believe the U.S. stock market is in the middle of a secular bull market, so maintain a long-term focus.

The bond market settled into a period of interest rate equilibrium. The Federal Reserve implemented its third and likely final 25 basis point rate cut for this year in late October. The new targeted fed fund rate of 1.50-1.75% is likely to hold well into 2020 as the Fed closely monitors economic activity. Any future rate moves by the Federal Reserve will be “data dependent”. The Fed’s three rate cuts this year have removed the near-term threat of an inverted yield curve. The slope of the yield curve now has a positive slope and a trading range for rates has been established. The 10-year U.S. Treasury finished the month yielding 1.78%, up 9 basis points on the month and 16 basis points below the highest monthly close of 1.94% on November 8th. The 2-year and 30-year closed the month yielding 1.62% and 2.21% respectively.

It has been a great year for investors with all asset classes showing significant year-to-date gains entering the final month of 2019. At these new record levels, it’s time for investors to seriously think about a strategy for managing portfolio success. A time tested tool which guides you to buy low and sell high over time is systematic portfolio rebalancing.

Take this opportunity of market strength to rebalance your portfolio back to your targeted risk tolerance. For example, if three years ago your long-term risk profile targeted your asset allocation to be 60% stocks and 40% bonds. Today, due to market fluctuations let’s assume your portfolio has changed to 72% stocks and 28% bonds. It’s likely an opportune time to rebalance. Use this strong market as an opportunity to reduce stocks by 12% and add 12% to bonds, thus returning your portfolio to the original 60/40 allocation target. Moving forward, set predetermined periods of time or percentages to active your portfolio rebalancing. This will remove any emotion from the buy/sell decision.

Rebalancing annually or when your allocation exceeds the target allocation by +/- 10% are both prudent strategies.

The main advantages to regularly rebalancing your portfolio are:

- Rebalancing stabilizes the risk level of your portfolio over time

- Creating a non-emotional process for selling the stronger performing asset class and buying the weaker performing one

- Making the decision to “go to cash” is eliminated, thus keeping your diversified portfolio fully invested over time

- Rebalancing provides a psychological satisfaction of taking action in a measured way

Systematically rebalancing your investment portfolio is a powerful tool that puts you in the driver seat and keeps the market noise in the back seat. If you have not implemented a rebalancing program, now is a perfect time to do so.

To expand on these Market Commentaries or to discuss any of our investment portfolios, please do not hesitate to reach out to us at 775-674-2222