The start of this New Year is eerily similar to the start of 2014. In atypical fashion, stock prices pulled back January only to rebound to new highs in February. The market’s so-called “January Effect” has taken a respite in recent years.

Is this a coincidence or will 2015 be a rerun of last year? In many ways the stock market environment is very similar to a year ago. Interest rates are low by historical standards, the U.S. economy shows modest positive growth, the economic outlook for international developed and emerging markets is flat, and geopolitical events continue to grab the headlines. From a valuation standpoint, forward price earnings ratios in the past year have expanded from about 15 times to 17 times forward earnings. Future price gains will be more difficult from these levels and will require stronger earnings growth in the upcoming quarters.

This earning’s season has not been spectacular, but the majority of companies reported results better than expected. The winners like Apple were rewarded and the losers like the energy sector were punished. Our call for the equity market in 2015 continues to be low single digits returns. Stocks will survive at these levels, but they will need a more robust global economic environment to prosper.

The bond market has entered a new era of extended low interest rates. Low interest rates will be the norm well into the foreseeable future. Demographics have created an insatiable appetite for fixed income investments as baby boomers try to protect principal and generate income for living expenses. The bond market will need to come to grips with a Federal Reserve that wants to raise short-term interest rates in a weak economic environment. We expect marginally higher short-term rates later this year with stable longer term interest rates. Expect two to four percent returns from the bond market this year.

2015 will be an emotionally challenged year for investors. Commitment to your financial plan while keeping market driven emotions removed from financial decision making process will make or break individual results. Remove the emotional panic button from the investment equation. If we get the much anticipated ten percent price decline, think buy more versus running to cash. The long-term investor will be rewarded. Embrace your financial plan and stay invested for the long haul.

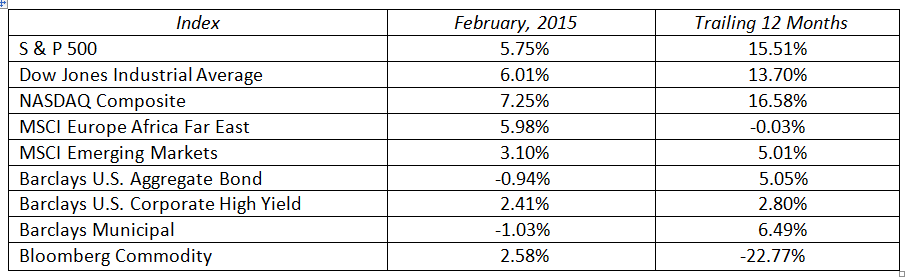

MARKETS BY THE NUMBERS: